Veteran health care journalist and author Marshall Allen tells the story of a 51-year-old man who needed two MRIs of his back. His nurse practitioner referred him to a nearby hospital-affiliated imaging center, where the MRIs would cost a total of $9,000, which he’d have to pay for out of pocket because his health plan deductible was $10,000.

The man wisely decided to check out the prices from other providers. At an imaging center about half a mile from the first one, the cost was $950 for both MRIs. In other words, “He got the same tests for more than $8,000 less by shopping around,” Allen says on his website. “That’s about what I paid for my last car—a huge savings.”

The situation may be surprising, but perhaps it shouldn’t be: The price of an MRI can vary by $300 to $3,000 in the same geographic area, with no demonstrated difference in quality.

Allen shared this story as an example of potential cost savings that are available. But comparison shopping for nonemergency care is just one of many smart tactics that can reduce health care costs for employers and their employees.

For business leaders coping with a range of fast-evolving workplace issues, the rising cost of health insurance remains a constant concern. Health care expenses have long outpaced both general inflation and wage increases, and there’s little relief in sight. Consumer prices—rising at the fastest pace in decades—are likely to push health benefits costs still higher this year and next.

In response, employers are boosting efforts to make benefits more affordable. At the same time, they’re elevating employee awareness of what benefits are offered and how best to access them.

For example, results released in April from consultancy WTW’s 2022 Emerging Trends in Health Care Survey showed that nearly two-thirds of more than 600 U.S. employers (64 percent) intend to take steps to address employee health care affordability over the next two years.

Most employers will try to avoid passing on increased costs “because of the tight labor market and the desire to keep health care affordable for employees,” says Jeff Levin-Scherz, population health leader at WTW. Still, employers’ total rewards budgets are limited, so increased health care spending could cut into funds set aside for other benefits costs—and pay raises.

That leaves employers with the difficult task of trying to keep their coverage expenses manageable without further straining employees’ financial well-being. To do that, they’ll need to identify and implement smart cost-management strategies.

Cost Trends Today

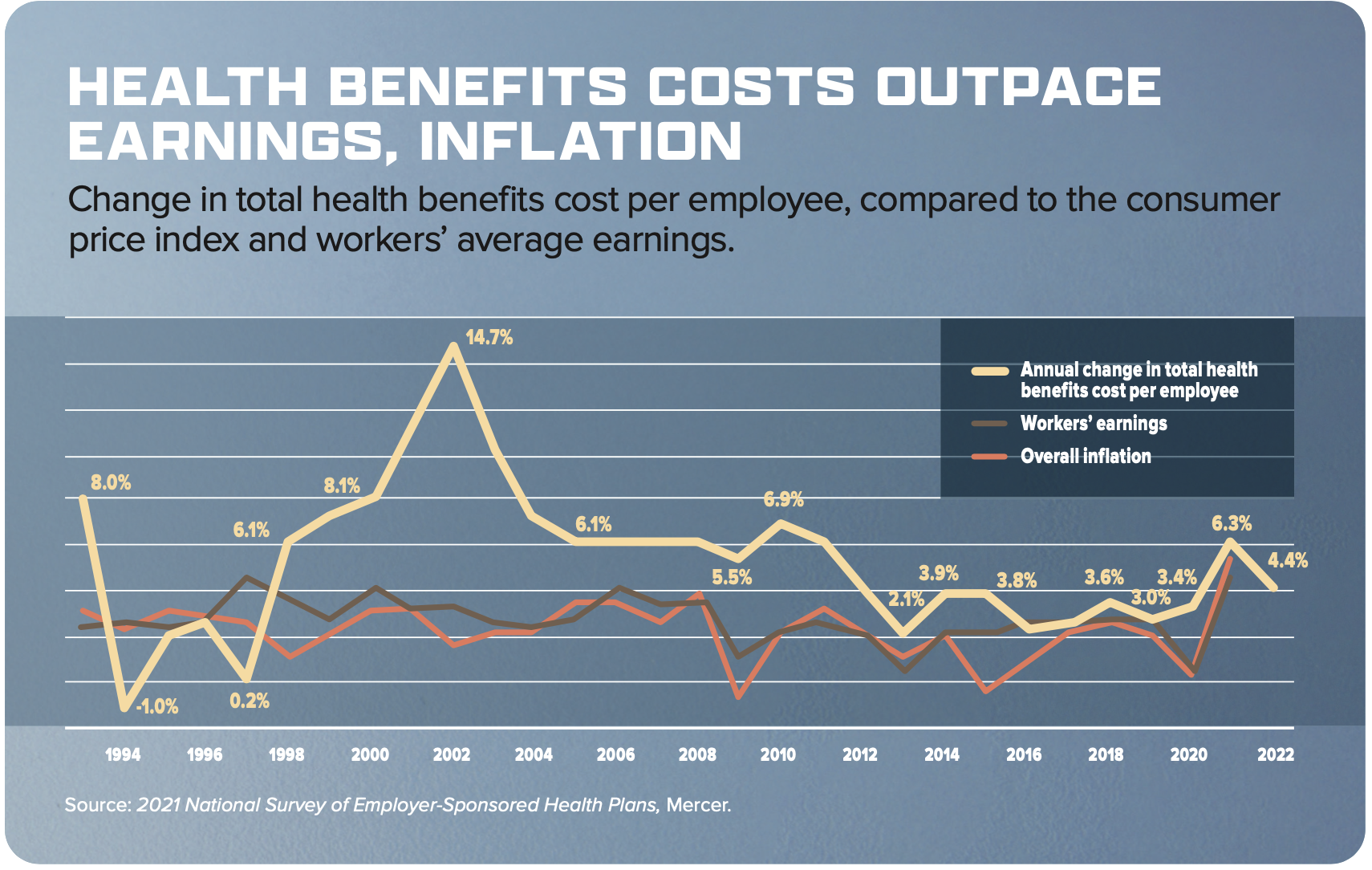

The average per-employee cost of employer-sponsored health insurance rose 6.3 percent in 2021, as employees and their families resumed seeking care after avoiding it during the height of the pandemic, HR consultancy Mercer’s 2021 National Survey of Employer-Sponsored Health Plans report found.

At the end of 2021, employers were projecting, on average, a fairly typical cost increase of 4.4 percent for 2022. The recent inflation spike, however, may upend those expectations.

Mercer’s chief actuary, Sunit Patel, cautioned that a number of factors could drive increased growth in health care costs as the pandemic wanes. “At the top of the list of concerns are higher utilization due to ‘catch-up’ care, claims for long COVID, extremely high-cost genetic and cellular drug therapies,” and the general effect of inflation on health care prices, he says.

Last year, health benefits cost growth was sharpest among smaller employers. Those with 50 to 499 employees saw a 9.6 percent increase, while larger employers (those with 500 or more employees) reported average cost growth of 5 percent.

Smaller employers usually offer fully insured health plans, with premium increases reflecting insurance carriers’ expectations of higher costs. Larger employers are more likely to sponsor self-insured plans, in effect acting as their own insurers, with more ability to control costs and plan design.

Meanwhile, prescription drug costs among large employers rose 7.4 percent last year, driven by an 11.1 percent increase in spending on high-cost specialty drugs.

Limits on Cost-Shifting

When health benefits cost growth accelerates, employers typically ratchet up cost-management efforts to keep increases at sustainable levels. However, one traditional tool—shifting a larger share of the cost of health services to plan enrollees—seems to be off the table for many employers. That’s because they’re mindful of the financial strain many employees are under.

Nearly half of insured adults say they have difficulty affording out-of-pocket costs and 1 in 4 have difficulty affording their deductible, according to a Kaiser Family Foundation (KFF) report based on a poll released late last year.

Concerns about health care affordability for lower-wage workers, along with the need to retain and attract employees in a tight labor market, have limited or even reversed some health plan cost-shifting trends. For instance, Mercer reported that in 2021:

Among small employers, the median deductible for individual coverage in a preferred provider organization plan dropped from $1,000 to $900.

Among large employers, the median individual deductible in a health savings account (HSA)-eligible high-deductible plan dropped from $2,000 to $1,850.

According to the KFF report, “Half of U.S. adults say they put off or skipped some sort of health care or dental care in the past year because of the cost, while 3 in 10 also report not taking their medicines as prescribed at some point in the past year because of the cost.”

Most employers want to keep money in their workers’ pockets. “Employees are already dealing with high financial exposures on their current health insurance plans, and they’re all pressed for money as well,” says Marcus Newman, vice president for benefits consulting at GCG Financial, an Alera Group company. “How much more risk can we ask them to shoulder?”

Medical expenses are already hampering many people in the U.S. Even among those with employer-provided health insurance, 61 percent reported carrying medical debt, according to a February 2022 survey by AffordableHealthInsurance.com, a health insurance website. Overall, nearly one-fourth (23 percent) of those with medical debt for out-of-pocket health bills owe more than $10,000. Many have delayed buying a house or saving for retirement because of the debt.

Medical expenses are already hampering many people in the U.S. Even among those with employer-provided health insurance, 61 percent reported carrying medical debt, according to a February 2022 survey by AffordableHealthInsurance.com, a health insurance website. Overall, nearly one-fourth (23 percent) of those with medical debt for out-of-pocket health bills owe more than $10,000. Many have delayed buying a house or saving for retirement because of the debt.

Newman suggests that employers explore strategies such as partially self-funded plans for small businesses, which, depending on the organization’s workforce demographics, may be more cost-effective than a fully insured plan. Another option is to make use of health reimbursement arrangements or HSAs to encourage plan participants to make cost-conscious spending choices when they’re able to do so, he says.

In a CFO Perspective on Health survey fielded by Mercer earlier this year, corporate chief financial officers (CFOs) and finance officers responsible for health care oversight indicated that over the next three years, they intend to strongly or very strongly emphasize cost-management strategies such as:

- Increasing clinical management with greater monitoring and oversight of care (cited by 58 percent of respondents).

- Using smaller, high-performing hospital and physician networks (48 percent).

“Plan-design changes generally shift cost to employees, and thus have a greater chance of causing dissatisfaction,” Patel says. “Given the tight labor market conditions, it’s understandable that CFOs would prefer strategies that don’t add to employees’ financial burdens.”

Cost-Management Features

While cost-shifting may have reached its limits, health benefits specialists agree on several plan-design measures that employers can adopt to help rein in rising costs.

According to Julie Stone, managing director of health and benefits at WTW, “rising costs and increased utilization, fueled by a resurgence in deferred care, are driving employers to find new ways to control costs while providing employees with affordable, high-quality care.”

Three-quarters of health insurers, for instance, say managing a health plan’s network of care providers is critical to controlling rising medical costs, according to WTW’s 2022 Global Medical Trends Survey of 209 leading insurers.

The plan features most likely to keep costs under control were:

- Contracting directly with high-quality, cost-competitive doctors and hospitals for in-network coverage (cited by 75 percent of respondents).

- Requiring preapproval for scheduled inpatient services (67 percent).

- Offering telehealth services (63 percent).

Telehealth or virtual care rose to the third spot on the list from the fifth position the previous year, “a sign that more insurers see potential savings from remote options for diagnosing and treating patients,” according to WTW.

“Telehealth’s momentum will be sustained post-pandemic,” predicts Francis Coleman, managing director at WTW. “The role of telehealth will continue to evolve not only as a navigation tool to speed access to the right care but also as a means to close gaps in access to care.”

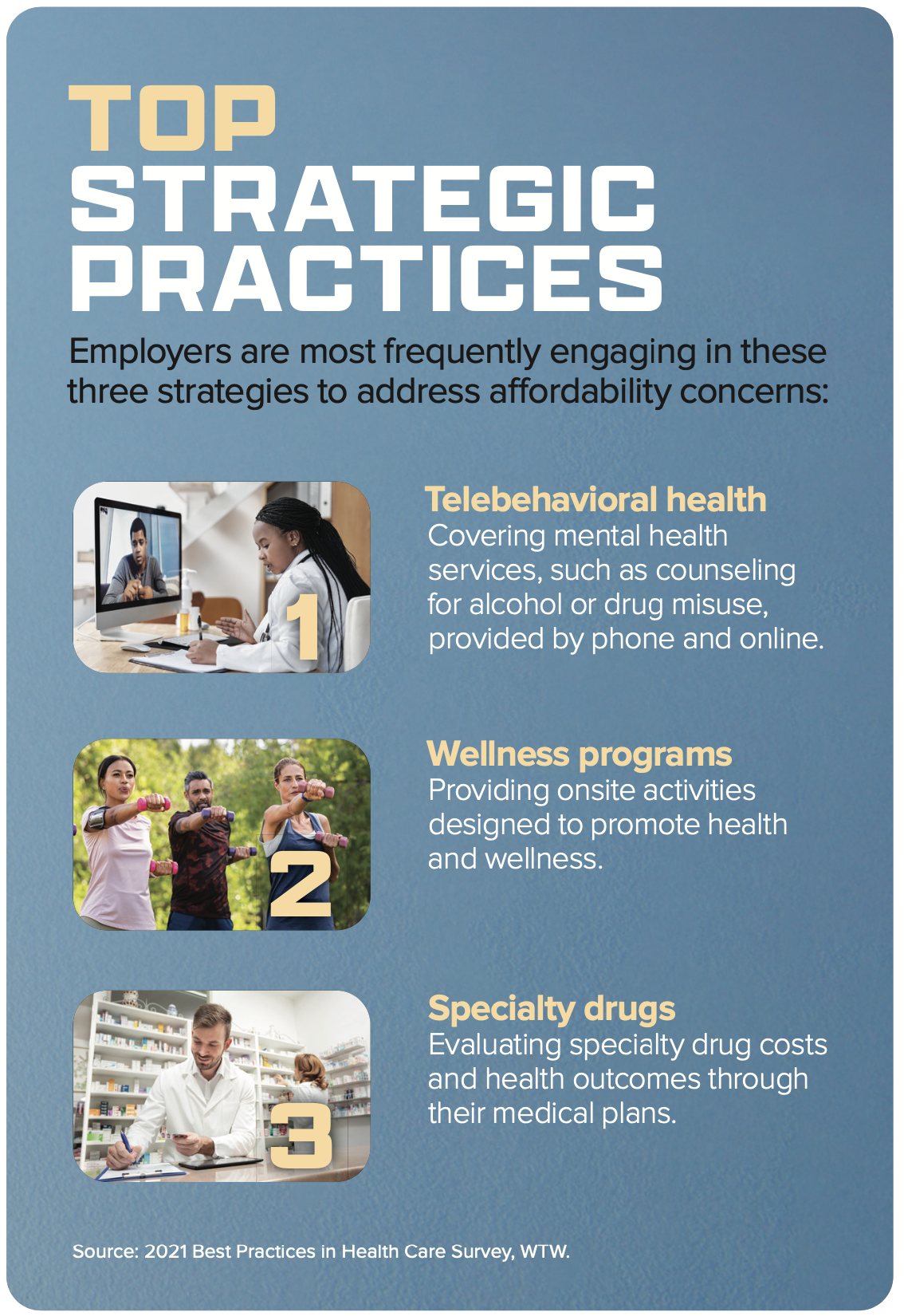

In companion research, the 378 U.S. employers that participated in WTW’s 2021 Best Practices in Health Care Survey identified the following measures as ones they’re taking to address affordability:

- Telebehavioral health. Eighty-nine percent of respondents are now offering coverage for telebehavioral mental health services, such as counseling for alcohol or drug misuse.

- Onsite wellness programs. Fifty-five percent offer worksite activities designed to promote health and wellness.

- Specialty drugs. Fifty-four percent evaluate specialty drug costs and health outcomes through their medical plans.

- Centers of excellence. Forty-eight percent use centers of excellence within their health plans. This means they pay a higher share of costs for coverage received at hospitals or clinics rated as offering high-quality, cost-effective care, often because they specialize in procedures such as joint replacement or conditions such as cancer.

- Concierge services. Thirty-one percent offer access to concierge services with integrated care-management programs.

- Working-spouse surcharges. Twenty-five percent impose spousal surcharges when additional employer-sponsored coverage is available for the working spouse.

- Differentiated premium contributions. Twenty-two percent base employee contributions on pay levels or job grades.

- Narrow networks. Twenty-one percent offer narrow networks that limit in-network doctors and hospitals to higher-quality health care providers with competitive costs for their services.

- Medication adherence. Thirteen percent provide support services to help ensure that employees take their medications as prescribed, which can help improve health outcomes, especially in more vulnerable populations.

Price Disclosure Initiatives

Federal regulations dictate that self-insured group health plans and insurance companies must provide plan enrollees with estimates of their out-of-pocket expenses for services from different health care providers through an online self-service tool; this allows enrollees to shop around and compare costs for services before receiving care. The final rule on transparency in coverage, issued in 2020 by the U.S. departments of Labor, Treasury, and Health and Human Services, will not take full effect until 2024.

The transparency rule will require plans and issuers to disclose in-network, provider-negotiated rates; historical out-of-network allowed amounts; and drug-pricing information.

The Consolidated Appropriations Act of 2021 also requires group health plans to report certain information related to health care and prescription drug costs to the secretaries of health and human services, labor, and the treasury. The first report is due by Dec. 27, 2022. The agencies will use the information to analyze trends in overall spending by group health plans, which could help insurers and self-insured plans negotiate fairer rates with health providers and lower costs for plan participants.

Help from Brokers

As cost-control challenges mount and transparency disclosures near, most benefits brokers report that employers want their help detailing the organizations’ health care spending and educating employees about why—and how—they should “shop” for care, according to a January/February 2022 survey by DirectPath, a benefits education, enrollment and health care transparency firm.

Brokers are responding. The survey shows that 86 percent currently provide some sort of health care transparency and clinical advocacy services to help clients keep their health care costs down.

Despite recent and upcoming regulations requiring health plans and hospitals to share pricing information, “most employees aren’t aware these resources exist, have no idea how to access them and are unclear on what to do with the information once they get it,” says Kim Buckey, DirectPath’s vice president for client services.

“When employees understand how much costs can vary and can compare prices, they’re able to make more-informed decisions that ultimately pass savings on to their employers,” Buckey says. “Employers are recognizing the importance of educating employees to become smart health care shoppers.”

Stephen Miller, CEBS, is an online writer/editor for SHRM who focuses on compensation and benefits.